Estate planning is fundamental to legal planning and essential to protecting a person’s autonomy by putting in writing what’s most important. Estate planning provides loved ones and the legal system with a detailed plan about the person’s wishes, which is especially important when it comes to critical decisions about medical care and well-being if incapacitated, and how to distribute assets on death.

Not only does estate planning confirm how assets will be distributed upon death, but it also provides loved ones with details about decisions to be made during a crisis and the legal authority to make those decisions. A good estate plan will include a legal document called a “Durable Power of Attorney” (DPOA). The DPOA names someone to manage financial affairs and make critical health decisions if the person is unable to do so; for example, due to a health issue such as dementia or stroke.

Not all assets pass under a will. Assets held in a trust will pass according to the terms of the trust. Other assets may pass through titling, such as joint ownership with the right of survivorship. With a right of survivorship, the surviving owner becomes the account owner in case of the other account holder’s death. Still other assets will be directed from the account owner to another upon death through a beneficiary designation, or a “pay on death’, or “transfer on death” designation. Even real property may avoid probate and pass from the owner to a beneficiary if the property is subject to a transfer on death deed.

Many securities like stocks, bonds, and assets in brokerage accounts or mutual funds are considered probate assets, absent other titling or direction. Further, funds in consumer bank accounts, like savings and checking accounts or money markets, are probate assets unless other titling or direction exists on the account. When a security or consumer bank account includes transfer provisions with a beneficiary designation, it is not an asset subject to direction through probate. Instead, the account passes virtually automatically on death. Generally, only a death certificate and completing a form is required to access the account and change titling to the new owner.

Real estate interests are typically considered probate assets. However, real estate interests often include certain complications based on ownership. Typically, real estate interests held as joint tenants with right of survivorship – meaning ownership is held by more than one party – results in the property becoming the sole property of the surviving owner after the other owner’s death. Other interests in property could include tenancy-in-common – meaning the deceased person’s share passes under their will and not to the other owner(s). Other property rights could include a life estate – meaning a right to possession of the real property during a lifetime. Other real estate may pass outside of property through a transfer on death deed. Especially with real estate, it’s important to understand how the property is held and put into place the right estate planning instrument, giving clear direction on ownership of the property following death.

And though not stated explicitly in the statute, pets are considered personal property, even though pets may be thought of as family members.

Even though personal property may be directed by way of a personal property list that accompanies a will, it is important to understand that titling of the asset, such as a car, may interfere with who actually owns the vehicle. For example, if there is debt on the car, the loan may need to be paid off before the vehicle can be distributed.

Life insurance policies and retirement accounts can also be considered probate assets under the right circumstances. For example, a life insurance policyholder can designate the policy’s assets to the beneficiary. However, if a beneficiary is not named, then the policy’s payout can be subject to probate. Further, retirement assets may be directionless, meaning that no one is chosen as a beneficiary of the account. However, the financial institution holding the retirement account may have a default beneficiary other than the estate. As a general rule, a good estate plan will not direct life insurance proceeds or retirement accounts to an estate. Instead, a designated beneficiary is preferred for creditor protection and tax minimization reasons.

Although every estate plan is different, virtually all plans include fundamental components – documents required for a complete estate plan. Below are the critical tools and components.

An Advance Directive is intended to be effective when a person has been diagnosed with a terminal illness or permanent vegetative condition. It is a legal document. For those who want to ensure they do not receive resuscitation attempts, a medical form known as a Physician’s Order on Life Sustaining Treatment (“POLST”) may be obtained from a doctor’s office. The POLST form should be prominently displaced, such as on the front of the refrigerator, so it is visible to emergency responders. Without a POLST, emergency responders and healthcare providers will attempt cardiopulmonary resuscitation (CPR) if the principal’s heart has stopped. CPR will only be withheld with a POLST stating DNAR (Do not attempt resuscitation).

A will is one of the most common estate planning instruments in the United States. A will details how a person wants their assets distributed upon death. A will only comes into effect upon a person’s death. The signer of the Will is called the testator (or “testatrix”).

The most common trust is a revocable living trust. It allows for continued management of trust assets while living and assignment of beneficiaries of the trust’s assets upon death.

A revocable living trust may be revoked at any time during the lifetime of the creator of the trust. The creator of the trust is called the “trustor.” The trustor transfers their assets into the name of the trust so that those assets are managed by the “trustee” for the benefit of the “beneficiary” according to the terms of the trust.

With revocable living trusts, it is common for the trustor, trustee, and beneficiary to all be the same person – at least initially. The trust provides for successor trustees to take over in the event of death or incapacity and directs the disposition of assets upon the trustor’s death.

A revocable living trust’s main benefit is avoiding probate. Managing assets during the trustor’s lifetime and after death is also a key benefit.

An irrevocable trust works differently. Unlike a revocable living trust, it may not be revoked. It is a complete divestment of assets by the trustor to the trustee for management of assets in the trust for its beneficiaries. Thus, the trustor no longer has ownership or control of the assets. Common reasons someone would create an irrevocable trust are for asset protection and tax mitigation. Tax liability will be paid by the trust unless the income is distributed out to beneficiaries, in which event the beneficiaries of the trust pay income tax on the income.

Irrevocable trusts can be excellent planning vehicles for Long-Term Care and Medicaid planning options.

Living trusts are created during lifetime. A living trust may be revocable or irrevocable. A living trust is called an “inter vivos” trust.

A testamentary trust is a trust that is created after a person has died and is typically created via a will. Testamentary trusts are often recommended for creation of trusts for minor children and grandchildren. Such trusts often end when the beneficiary child reaches a certain age.

Other testamentary trusts may continue for the lifetime of the beneficiary and for future generations, such as a dynasty trust.

If Long-Term Care costs are a concern, a couple may use a testamentary special or supplemental needs trust to protect assets for the surviving spouse against Long-Term Care costs without those assets in the trust interfering with Medicaid benefits.

A spendthrift trust provision protects trust assets for the beneficiary, preventing the beneficiary from assigning or selling their beneficial interest in the trust’s assets. Instead, the trustee maintains and controls the trust assets and distributes assets to the beneficiary only according to the terms of the trust. So, the assets will be protected from the beneficiary’s creditors.

This trust is designed to provide assets to a beneficiary who is disabled or who receives needs-based government benefits. Parents of children with special needs often set up these trusts, either during their lifetimes or through their wills, to ensure assets are available for the child’s care and to enhance quality of life. Special needs trusts are incredibly important to preserve the disabled child’s eligibility to receive government benefits.

Federal and state social welfare programs like Medicare, Medicaid, and Social Security Disability may terminate benefits to recipients based on income and asset levels. Often, an inheritance of assets dramatically raises the beneficiary’s resource threshold, thereby making them ineligible for benefits. Thus, a special needs trust preserves those assets for future care without jeopardizing eligibility for government benefits.

Probate is the legal process to administer an estate under the authority of the court. After the will is filed with the court, the personal representative, also known as the “executor” is appointed and is granted the legal authority to act on behalf of the estate through issuance of Letters Testamentary. Probate is a well-defined procedure for the orderly administration of an estate and ensures debts are paid, assets distributed according to the testator’s wishes, and is useful in protecting assets and extinguishing certain creditor’s claims.

When a person decides to establish a structure for their estate in the event of their death, the person typically appoints a designated estate representative to supervise the execution of the legal instruments guiding the estate. Because many estates involve smaller and less complicated assets, the average person with no formal legal or financial training can serve as a representative. However, estates worth millions of dollars with numerous asset classes should be handled by an appointed attorney or accountant. In instances where the testator executed no legal instrument, the probate court overseeing the estate can appoint an estate representative to oversee the distribution of assets.

The probate process can seem complicated and confusing. The steps to administer probate are statutorily mandated and must be followed correctly. However, with the proper legal guidance and support, the personal representative will be able to carry out the decedent’s wishes are stated in their will.

It’s important to note that even if there is no will, the decedent’s estate will be subject to probate unless their estate plan included a legal plan to avoid probate, such as use of a revocable living trust or transfer on death direction of assets. Generally, however, if there’s no estate planning documents in place, the administration of the estate will be more complicated and difficult. The laws of intestacy will apply and the state’s plan for distribution of assets will be followed. Additional costs, legal fees, and disputes among those who inherit may be present where the estate is being probated under the laws of intestacy.

To open probate a petition is filed with the court. The petition is verified by the person seeking to be the personal representative that the facts stated are true. The petition asks the court to recognize the will as properly executed and valid and appoint the designated person to serve as personal representative/executor as the estate. If the decedent did not have a will, Washington law has a process to help courts determine the executor, which includes the surviving spouse or children.

After probate has opened, the executor must notify relevant parties to the estate that an appointment has been made of the executor. This notice allows relevant parties to contest the appointment. Those notified should include beneficiaries and heirs-at-law. Once the challenge period ends, no relevant party or heir can directly challenge the appointed executor. However, malfeasance by the executor may lead to their removal.

The executor must notify certain government entities of the probate. Typically, the funeral home will have notified social security of the death so any benefits will cease. The Washington Department of Revenue and Office of Financial Recovery will also be notified.

One of the primary responsibilities of the executor is to gather information about all assets owned by the decedent and inventory those assets so they can be properly distributed or addressed during probate. This includes liquid assets, real property, tangible property, life insurance policies, retirement accounts, and other securities. The executor should inspect the decedent’s safes, safety deposit boxes, and personal items. Once all assets have been located and inventoried, the executor can determine the final dollar figure of the asset, start dividing the assets and assess tax and other liabilities.

After fully accounting assets, the executor should find all debts owed by the decedent. An estate can only be lawfully distributed once creditors have been paid, or the claim of a creditor has been determined invalid. Taxes, including income and estate taxes, must be included in determining what is owed and what must be paid before distributions of estate assets occur.

The executor should follow the proper notice procedure. Actual creditors, meaning those known to the executor, should be notified of the probate. Publication of notice to unknown creditors reduces the time frame that unknown creditors can assert a claim against the estate to four months. A creditor who is ascertainable, but who did not receive actual notice has two years to file a claim against the estate for any outstanding liability.

During probate, an executor is charged with maintaining all assets. Although some assets, like tangible property and liquid assets, stay static during probate, others do not. Therefore, the executor’s responsibility is to protect assets during probate. For example, an executor will need to continue insurance coverage on real property, may continue to collect rent from income property or fix damage to real estate assets, etc. during probate.

Once all assets have been fully accounted for and valid debts have been addressed, the executor can begin disbursing the assets according to the terms of the will. Once their distribution is received, the beneficiary must sign a receipt that they have received their proper distribution.

Finally, the executor is ready to close the probate. Typically, such closure is done through filing with the court of a Declaration of Completion and notice or waiver of notice to the estate beneficiaries. A beneficiary has 30 days to contest the closing of the probate. If no objection is made, the proceeding closes.

If you or your loved ones are in need of a Spokane estate planning attorney in contact ELG Estate Planning for more information.

Compassion and respect: two words that drive ELG Estate Planning to provide capable Estate Planning and Elder Law services for our clients. Regardless of age, no one likes to think about the possibility of being incapacitated, or of what will happen to your loved ones when you are gone. We at ELG Estate Planning understand the stresses and complexities that come from life’s journey. Many on our Team have cared for our own aging loved ones, and we know the confusion and fear that arise when physical and mental abilities fade. We understand the importance of caring for those who are important to us, be it an aging parent or a child or grandchild.

We’ve seen how a well-thought-out Estate Plan can mean the difference between ease and comfort versus chaos and impoverishment where there was no plan, or a bad plan. ELG Estate Planning provides what you need: resources and a plan to give you the best life possible.

At ELG Estate Planning we are here to provide you the information you need. Questions about Estate Planning? Wills? Trusts? Durable Powers of Attorney? Health Care Directives? Caring for a loved one? Paying for care without going broke? What do you need? What steps can you take to protect yourself, your family and your money?

A Will with an Asset Protection Trust protects assets for a surviving spouse or any beneficiary. To allow for flexibility, funding of the Trust can either be mandatory or contingent. If contingent, upon the death of the first spouse, a decision will be made at that time whether to protect assets through funding the Asset Protection Trust for the surviving spouse with the deceased spouse’s assets. Importantly, the Asset Protection Trust shields assets from unnecessary depletion. Assets in the Trust are not considered “countable” by Medicaid or other government needs-based benefit programs. Thus a Will with an Asset Protection Trust avoids depleting funds unnecessarily, and is especially useful if expensive Long-Term Care is needed by the surviving spouse. Couples can protect 50% to up to 100% of their estate from Long-Term Care expenses, creditors, and the State.

A Will with an Asset Protection Trust not only protects assets for the surviving spouse, but also for other beneficiaries should they need asset protection at the time they inherit. Furthermore, assets that remain in the trust ultimately will be distributed according to the wishes of the first spouse to pass, thus avoiding “unintentional disinheritance” of your beneficiaries due to unforeseen future events, such as remarriage.

“Special Needs” or “Supplemental Needs” describes any trust intended to provide benefits without causing the beneficiary to lose public benefits he or she may be entitled to receive.

When individuals with special needs who receive government needs-based benefits receive money from personal injury settlements, inheritances or other sources, they can lose their public benefits. You can structure your estate so that you provide assistance to your disabled child or grandchild without jeopardizing their receipt of benefits. This also can include a surviving spouse who may need Long-Term Care. Such a trust preserves those benefits and sets aside additional funds for the person with special needs. For a surviving spouse needing Long-Term Care, such a trust renders those assets non-countable for Medicaid qualification.

It depends. Both terms can be interchangeable, and describe the purpose of the trust rather than being a limited legal term. However, the term “Special Needs” trust commonly is used to refer to a trust that a disabled person creates for themselves, or to a trust created for a disabled child. A “Supplemental Needs” trust often refers to a trust created by a third-person for someone, like a spouse or child, who would benefit from asset protection, though who would not be referred to as a person with “special needs”.

No. The existence of a Special or Supplemental Needs Trust does not itself make public benefits available. The beneficiary must meet eligibility criteria to qualify for the benefits program. If properly drafted and established, funds in the trust will not cause a loss of benefits.

A Revocable Living Trust is an arrangement for the management and distribution of your property. Such an arrangement is revocable during your lifetime. Your assets are transferred to the Trustee of the Revocable Living Trust, who manages and distributes the property according to the terms of the trust. The grantor/trustor, meaning the person who creates the trust, often serves as their own Trustee.

A Revocable Living Trust can be a good Estate Planning tool for those who own property in other states. However, unless it is properly funded and administered, upon the Trustor’s death there will need to be both a trust administration and a probate. A primary goal of a Revocable Living Trust is to avoid probate, especially in states such as California where probate is expensive and complicated – which is not the case in Washington.

Also, it is very important to understand that Revocable Living Trusts provide no Long-Term Care Medicaid planning benefit for a surviving spouse in Washington. In fact, Revocable Living Trusts can prove harmful to asset protection and Long-Term Care benefits planning in Washington. It is important to consult with an Elder Law attorney if you have or are considering a Revocable Living Trust.

Learn how to secure the future for both you and your loved ones. In these webinars, Managing Partner Lynn St. Louis will teach you the ins and outs of estate planning to ensure your family is taken care of.

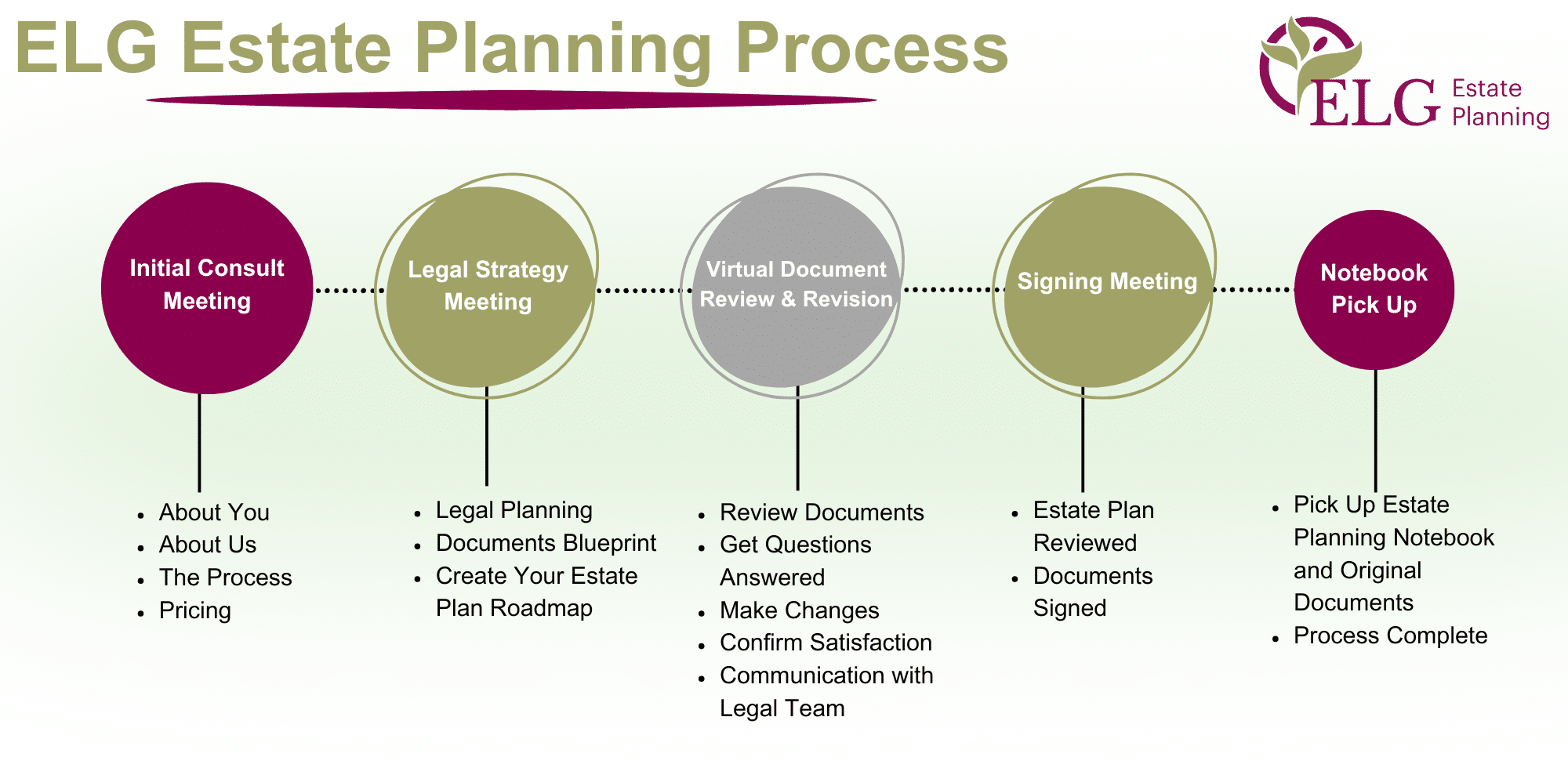

With an experienced Spokane estate planning attorney, you will have a guide through every step of securing your future. We’re happy to answer any questions and ensure you understand the decisions before you.

Your estate plan will be crafted with a Spokane estate planning attorney at your side every step of the way. You’ll have the confidence in knowing that your future and that of your loved ones is secured.

The first step to a successful Estate Plan is simple: reach out and learn more from a trusted Spokane estate planning attorney on our team. We have helped thousands of clients get started in estate planning Spokane, Washington. Understanding your goals and your concerns about family estate planning is what is most important. Everyone’s situation is unique. Find out how we can help you get your plan in place for what matters most to you.